Our News

Our News

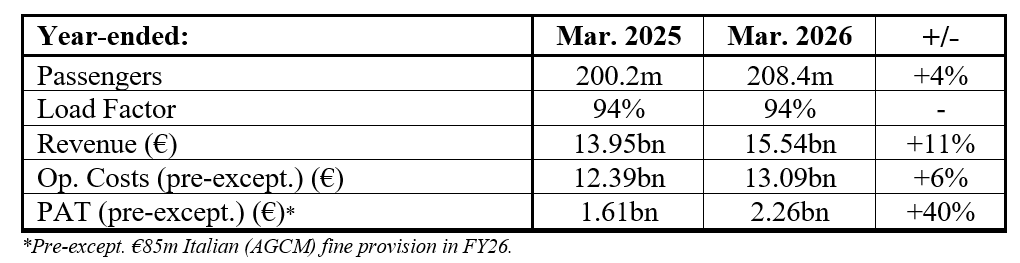

RYANAIR 2025-26 PAT RISES 40% TO €2.26BN (PRE-EXCEPT.) TRAFFIC GROWS 4% TO 208M DESPITE BOEING DELAYS

Ryanair Holdings plc today (18 May) reported record full-year (FY26) PAT of €2.26bn (pre-exceptional) up 40% over its prior-year PAT of €1.61bn.

FY26 highlights include:

- Traffic grew 4% to 208.4m, despite delivery delays on 29 B-8200 aircraft.

- Rev. per pax up 7%.

- Unit costs rose 1% (pre-except. charge).

- FY27 jet-fuel 80% hedged @ $668 met. tn.

- All 210 B737 “Gamechangers” in 647 fleet at 31 Mar.

- 30 spare LEAP-1Bs purchased.

- Final div. of €0.195 per share payable in Sept. (subject to AGM approval).

Ryanair Group CEO Michael O’Leary, said:

Revenue & Costs:

“Group revenue rose 11% to €15.54bn. Scheduled revenue increased 14% to €10.56bn as traffic grew 4% with 10% higher fares (recovering last year’s 7% fare decline). Ancillary revenue rose 6% to €4.99bn (€24 per pax). Operating costs (pre-exceptional) rose 6% to €13.09bn (+1% per pax). With all 210 B-8200 “Gamechangers” now delivered, other income fell reflecting significantly lower delivery delay compensation in FY26. While our lawyers are confident that the baseless Italian AGCM fine levied in Dec. 2025 will be overturned on appeal, an exceptional €85m provision (approx. 33% of the €256m fine) is included as an exceptional charge in the FY26 results.

Jet-Fuel Hedging:

The conflict in the Middle East has created economic uncertainty and we still don’t know when the Strait of Hormuz will reopen. Despite this, Europe remains relatively well supplied with jet-fuel, with significant volumes sourced from West Africa, the Americas and Norway. Global jet-fuel spot prices have, however, spiked to over $150bbl and are expected to remain elevated versus pre-conflict levels for some months. Ryanair’s conservative jet-fuel hedging strategy (80% of FY27 jet-fuel is hedged at approx. $67bbl – to April 2027) will insulate Group earnings in the current very volatile oil markets and widen the cost advantage over EU competitors for the remainder of FY27.

Balance Sheet, Liquidity & Returns:

Our balance sheet is strong with a BBB+ credit rating (both Fitch and S&P) and an unencumbered B737 fleet of 620 aircraft. At 31 Mar. (year-end) gross cash was €3.6bn after €1.9bn capex spend, €1.2bn debt repayments and over €900m shareholder distributions. Liquidity is further boosted by the Group’s RCF which has c.€1bn undrawn. Net cash was €2.1bn, which enables the Group to repay its last €1.2bn bond next week leaving our group effectively debt free. This financial strength further widens the cost gap between Ryanair and our competitors, many of whom are exposed to expensive (long-term) finance, rising aircraft lease costs and unhedged jet-fuel.

During FY26, we purchased (and cancelled) some 2% of issued share capital (over 20m shares) and have now retired c.38% of Ryanair’s issued share capital since 2008. In line with our capital allocation policy, a final dividend of €0.195 per share is payable in Sept. (subject to AGM approval). Over the coming year, our priorities include the May repayment of our last €1.2bn bond, funding our MAX-10 aircraft capex, our dividends and the balance of our (€750m) buyback programme from internal cashflows while rebuilding the Group’s gross cash back to €4bn.

FLEET & GROWTH

The Group’s year-end fleet of 647 aircraft (incl. all 210 Gamechangers) should facilitate 4% traffic growth to approx. 216m this year (FY27). Boeing expect MAX-10 certification in late summer 2026 and have confirmed they expect to deliver Ryanair’s first 15 MAX-10s in Spring 2027 (in line with contract dates), with 300 of these fuel-efficient aircraft (20% less fuel & 20% more seats) due to deliver by Mar. 2034.

Building on last year’s deal to buy 30 new CFM LEAP-1B engines, in Q4 Ryanair agreed a multi-year engine material services agreement to purchase CFM parts (both CFM56-7B and LEAP-1B) to support the Group’s 2 engine shop (MRO) project which will bring all of Ryanair’s engine maintenance in-house. The first of these MROs are expected to be operational in early 2029 and we expect to identify the first location shortly. Our second MRO should be operational in early 2030s. When built, these 2 MROs will further widen the maintenance cost advantage that Ryanair has over competitor airlines.

Demand (despite the current Middle East conflict) remains robust, although the booking window is closer-in than last year. Ryanair has 130 new S.26 routes on sale (incl. new bases in Rabat, Tirana and Trapani). Our scarce FY27 capacity growth is allocated to those regions and airports who have cut aviation taxes and are incentivising traffic growth (such as Albania, Italy, Morocco, Slovakia and Sweden) as we switch flights and routes away from uncompetitive high tax markets like Austria, Belgium, Germany and Regional Spain. With near term fuel prices likely to remain high, we urge all passengers book early on www.ryanair.com to secure the lowest airfares for S.2026 travel.

We expect European short-haul capacity to remain constrained until at least 2030 as the 2 big OEMs remain well behind on aircraft deliveries, Pratt & Whitney engine repair delays continue, EU airline consolidation accelerates and unprofitable airlines (further hit by high jet-fuel prices) have recently withdrawn capacity due to unhedged fuel costs which leaves them less able to compete with Ryanair’s much lower costs. Industry capacity constraints, combined with our widening cost advantage, strong balance sheet, low-cost (fuel-efficient) aircraft orderbook and industry leading ops resilience will, we believe, facilitate Ryanair’s profitable growth to over 300m passengers p.a. by FY34.

CEO CONTRACT & BOARD UPDATE

This Spring the Board commenced discussions with Michael O’Leary (“MOL”) on an extension of his employment contract with the Group (currently ends 2028) until April 2032. These discussions have almost concluded and engagement with the Group’s largest institutional shareholders will commence in the coming days. Under the proposed new contract, MOL will have a purchase option over 10m shares struck at market price (before the recent Iran war related decline), but (similar to his 2019 grant) these options will only be exercisable if very ambitious PAT or share price growth targets are achieved, which will create substantial value for all shareholders. A further update will be provided in due course.

Following a period of significant Board refreshment, Stan McCarty (Chairman) and Róisín Brennan (SID) have agreed to remain on the Board until Sept. 2029 & 2030 respectively to facilitate experienced management of the Group, orderly succession and onboarding of new NEDs.

ESG

Our significant investment in new technology and operational resilience, coupled with ambitious SAF commitments, positions Ryanair as one of Europe’s most environmentally efficient airlines. During FY26 we took delivery of 34 new Gamechangers (4% more seats, 16% less fuel & CO2) and 30 new spare LEAP-1B engines, while accelerating the retrofit of winglets to 75% of our B737NG fleet (1.5% lower fuel burn and 6% less noise). The Group also recorded a record 89% CSAT score (PY: 86%). In recognition of the above, CDP (Carbon Disclosure Project) recently upgraded Ryanair’s climate rating to A (previously A-), MSCI reconfirmed the Group’s ‘A’ rating and Sustainalytics graded the Group as “low-risk”.

OUTLOOK

We expect FY27 traffic to grow 4% to 216m passengers. While 80% of our FY27 jet-fuel requirements are hedged at c.$67bbl (lower than prior year), the price of our unhedged 20% has spiked due to the Middle East conflict. Our EU enviro. taxes are expected to rise by a further €300m this year to c.€1.4bn which makes EU air travel even less competitive. With maintenance costs rising (ageing NG fleet and mid-life “hospital visits” on B-8200 LEAP engines) and some significant crew pay increases agreed under newly negotiated multi-year CLAs, if unhedged fuel prices remain at current elevated levels then FY27 unit costs could rise by a mid-single digit percentage. To date, S.26 travel demand remains robust although bookings are closer-in than last year reducing visibility. Pricing in recent weeks has eased somewhat in response to economic uncertainty caused by higher oil prices, the fear of fuel shortages and the risk of inflation adversely impacting consumer spending. As always, Ryanair will pursue its “load-active/yield passive” strategy to drive traffic growth, ancillary revenue and lower unit costs. With the first week of Easter falling into Mar. (benefitting Q4 FY26), we now expect Q1 fares to be behind (mid-single digit percentage) Q1 FY26 (which enjoyed a full-Easter). With constrained EU short-haul capacity, we had originally expected S.26 fares to rise modestly (low single digits) ahead of last year. Q2 pricing (with limited visibility) is now trending broadly flat and the final outcome will be totally dependent on close-in peak S.26 bookings and fares. With zero H2 visibility and significant fuel price/potential supply volatility it is far too early to provide any meaningful FY27 profit guidance at this time.

The final FY27 outcome remains heavily exposed to adverse external developments, incl. conflict escalation in the Middle East and Ukraine, risks to fuel supply shortages, higher for longer fuel prices on our unhedged 20%, macro-economic shocks and European ATC strikes & mismanagement. We hope to be able to give shareholders a clearer picture on H1 pricing and fuel costs during our Q1 results release in late July.”

Related News

RYANAIR LAUNCHES PRAGUE – PAPHOS & KOSICE ROUTES

Ryanair, Europe’s No.1 airline, today (1st August) celebrated the first flight from Prague to Paphos, while on Monday (3rd August) it will launch a twice weekly service to Kosice, both as part of its extended Summer 2020 schedule.

To celebrate its new routes, Ryanair has launched a seat sale with fares from 729 Kc for travel to Kosice and from 759 Kc to Paphos, both until the end of October, which must be booked by Wednesday (5th August), only on the Ryanair.com website.

RYANAIR LAUNCHES PRAGUE – PAPHOS & KOSICE ROUTES

Ryanair, Europe’s No.1 airline, today (1st August) celebrated the first flight from Prague to Paphos, while on Monday (3rd August) it will launch a twice weekly service to Kosice, both as part of its extended Summer 2020 schedule.

To celebrate its new routes, Ryanair has launched a seat sale with fares from 729 Kc for travel to Kosice and from 759 Kc to Paphos, both until the end of October, which must be booked by Wednesday (5th August), only on the Ryanair.com website.