Our News

Our News

RYANAIR REPORTS PAT OF €1.61BN DESPITE 7% LOWER FARES 1ST EU AIRLINE TO CARRY 200M GUESTS IN ONE YEAR

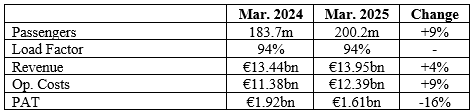

Ryanair Holdings plc today (19 May) reported full-year profit after tax of €1.61bn, compared to prior-year PAT of €1.92bn, as traffic grew 9% to a record 200m passengers at 7% lower fares.

FY25 highlights include:

- Traffic grew 9% to a record 200m, despite Boeing delivery delays.

- Ave. fare down 7% & ancil. revenue up 1%.

- Cost per pax flat as the cost gap widens over competitor EU airlines.

- 181 B737 “Gamechangers” in 618 fleet at 30 Apr.

- Over 160 new routes for S.25.

- 7% of shares bought back & cancelled.

- Final div. of €0.227 per share payable in Sept. (subject to AGM approval).

FY25 BUSINESS REVIEW

Ryanair Group CEO Michael O’Leary, said:

Revenue & Costs:

“The key feature of last years result was the 7% decline in fares which drove strong traffic growth of 9% to just over 200m. Total revenue rose 4% to €13.95bn. Scheduled revenue increased 1% to €9.23bn as traffic (despite repeated Boeing delivery delays) grew 9%. The absence of a full Easter in Q1, consumer spending pressure (driven by higher-for-longer interest rates and inflation in H1) and a big drop off in OTA bookings prior to S.24 necessitated repeated price stimulation last year. Ancillary revenues were solid rising 10% to €4.72bn. Operating costs (flat on a per passenger basis) were in line with expectations, rising 9% to €12.39bn as fuel hedge savings offset higher staff and other costs due (in part) to repeated Boeing delivery delays.

Our FY26 fuel is almost 85% hedged at $76bbl and FY27 is 36% hedged at just under $66bbl which helps de-risk the Group from fuel price volatility.

Balance Sheet & Liquidity:

Ryanair’s balance sheet is one of the strongest in the industry with a BBB+ credit rating. At 31 Mar., gross cash was almost €4bn, boosted by delayed aircraft capex into FY26. Year end net cash was €1.3bn even after €1.6bn capex and €1.5bn of share buybacks. In Mar., the Group enhanced its financial flexibility by increasing its low-cost revolving credit facility to €1.1bn (was €0.75bn) and extending the term to Mar. 2030 (from 2028). Our owned B737 fleet (over 590 aircraft) is fully unencumbered, widening Ryanair’s cost advantage over all competitors. While Ryanair prepares to repay almost €2.1bn maturing bonds over the next 12-months from internal cash resources, our competitors remain exposed to expensive (long-term) finance, and rising aircraft lease costs.

Shareholder returns:

During FY25, Ryanair purchased and cancelled 7% of its issued share capital (over 77m shares) and has now retired almost 36% of its issued share capital since 2008. In line with our capital allocation policy, €0.40 cum. dividends per share were paid during FY25 and a final dividend of €0.227 per share is due in Sept. (subject to AGM approval). Over the next year, we intend to pay down maturing bond debt (incl. an €850m bond in Sept. 2025 & €1.2bn in May 2026) while still funding our aircraft and engine capex from internal resources. The Board remains committed to shareholder returns and has now approved a follow-on €750m share buyback, which will likely run over the next 6 to 12 months.

FLEET & GROWTH

Ryanair now has 181 B737-8200 “Gamechangers” in its 618 aircraft fleet (up 5 from year-end). This will restrict our FY26 growth to just 3% (206m passengers). We are working closely with Boeing to accelerate deliveries and are increasingly confident that the remaining 29 Gamechangers in our 210 orderbook will deliver well ahead of S.26, enabling us to catch up delayed traffic growth into FY27. Boeing expects the MAX-10 to be certified in late 2025 and so we continue to plan for the timely delivery of our first 15 MAX-10s in spring 2027 (with 300 due by Mar. 2034).

We are seeing robust S.25 travel demand across our network. This year our constrained capacity growth is being allocated to those regions and airports who are abolishing aviation taxes and incentivising traffic growth. Ryanair has over 160 new S.25 routes (total 2,600 routes) on-sale and we recommend all passengers book early on www.ryanair.com to secure the lowest airfares before they sell out.

We expect European short-haul capacity to remain constrained for the next few years as many of Europe’s Airbus operators are still working through Pratt & Whitney engine repairs, the big 2 OEMs are well behind on aircraft deliveries, and EU airline consolidation continues (incl. the upcoming sale of TAP). These capacity constraints, combined with our substantial cost advantage, strong balance sheet, low-cost aircraft orders and industry leading operational resilience will, we believe, facilitate Ryanair’s controlled profitable growth to 300m passengers p.a. by FY34.

ESG

During FY25 we took delivery of 30 Gamechangers (4% more seats, 16% less fuel & CO2) and we accelerated the retrofit of winglets to our B737NG fleet (target of 409 by 2026), which reduce fuel burn by 1.5% and noise by 6%. This investment in new technology, and our ambitious SAF commitments positions Ryanair as one of Europe’s most environmentally efficient airlines. This year we retained our industry leading ESG ratings from MSCI (A), CDP (A-) and Sustainalytics (No.1 global large cap airline). We also became the first major airline to have its environmental targets (to reduce CO2 per pax/km by 27% to c.50grams by 2031) validated to the latest SBTi guidelines. As we head into S.25, we continue to call on ATC CEOs across Europe to ensure adequate staffing, particularly for the morning/first wave departures. This, coupled with the protection of overflights (during national strikes), would deliver significant environmental and punctuality benefits for EU air travel.

Ownership & Control:

Between Sept. 2024 and Mar. 2025, in anticipation of reaching the 50% threshold of EU ownership, Ryanair carried out a review of a potential variation of its ownership and control restrictions in a manner that continues to ensure compliance with EU Reg. 1008/2008 (“O&C Review”). Once the 50% threshold was reached, the Board, taking into account positive feedback from regulators and investors resolved in March that it was in the best interest of Ryanair and our shareholders as a whole to discontinue the prohibition on non-EU nationals acquiring Ordinary Shares with immediate effect. We continue to apply voting restrictions on non-EU nationals. Consequently, both EU and non-EU nationals can now invest in Ryanair Holdings plc via Ordinary Shares listed on Euronext Dublin and/or Depository Shares listed on Nasdaq. In acknowledgement of these changes, MSCI recently confirmed Ryanair’s inclusion in the MSCI World Index at the end of May.

Board:

Howard Millar has chosen not to seek re-election at the upcoming AGM and will step down from the Board in Sept. We thank him sincerely for his leadership and his enormous contribution to Ryanair’s success, firstly as our CFO from 1992 to 2014, and as a NED over the last 9 years.

OUTLOOK

We expect FY26 traffic to grow by just 3% to 206m passengers due to constrained/delayed Boeing deliveries. Following a year of flat unit-costs, we expect modest unit cost inflation in FY26 as the delivery of more Gamechangers, strong jet fuel hedging and cost control across our Group airlines helps offset increased route & ATC charges, and higher enviro. costs (following the unwind of free ETS allowances and the introduction of a SAF blend mandate from Jan. 2025). To date, S.25 demand is strong, with peak fares trending (modestly) ahead of prior year. Q1 fares will benefit from having a full Easter holiday in April, and weak prior-year comps., and Q1 fares are on track to finish a mid-high teen percent ahead of Q1 FY25. With limited visibility, we currently expect Q2 pricing to recover some of the 7% decline we experienced in PY Q2. The final H1 outcome is, however, heavily dependent on close-in bookings and peak summer yields. As is normal at this time of year, we have zero H2 visibility.

While we cautiously expect to recover most, but not all of last years 7% fare decline, which should lead to reasonable net profit growth in FY26, it is far too early to provide any meaningful guidance. The final FY26 outcome remains heavily exposed to adverse external developments, incl. the risk of tariff wars, macro-economic shocks, conflict escalation in Ukraine and the Middle East and European ATC mismanagement/ short staffing.”

Related News

RYANAIR LAUNCHES PRAGUE – PAPHOS & KOSICE ROUTES

Ryanair, Europe’s No.1 airline, today (1st August) celebrated the first flight from Prague to Paphos, while on Monday (3rd August) it will launch a twice weekly service to Kosice, both as part of its extended Summer 2020 schedule.

To celebrate its new routes, Ryanair has launched a seat sale with fares from 729 Kc for travel to Kosice and from 759 Kc to Paphos, both until the end of October, which must be booked by Wednesday (5th August), only on the Ryanair.com website.

RYANAIR LAUNCHES PRAGUE – PAPHOS & KOSICE ROUTES

Ryanair, Europe’s No.1 airline, today (1st August) celebrated the first flight from Prague to Paphos, while on Monday (3rd August) it will launch a twice weekly service to Kosice, both as part of its extended Summer 2020 schedule.

To celebrate its new routes, Ryanair has launched a seat sale with fares from 729 Kc for travel to Kosice and from 759 Kc to Paphos, both until the end of October, which must be booked by Wednesday (5th August), only on the Ryanair.com website.