Our News

Our News

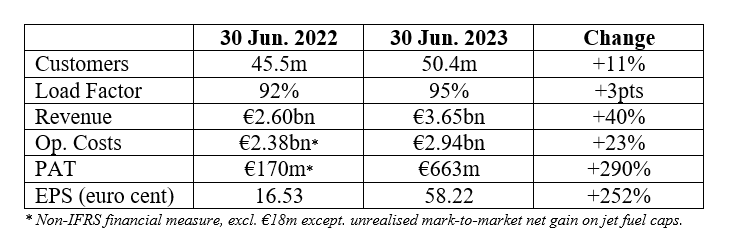

RYANAIR REPORTS Q1 PROFITS OF €663M

STRONG EASTER AND WEAK PRIOR YEAR COMPS. DUE TO UKRAINE INVASION

Ryanair Holdings today (24 July) reported Q1 profits of €663m, compared to a Ukraine affected prior year Q1 PAT of €170m thanks to a strong Easter, the extra UK (Coronation) public holiday in May and weak PY comps. due to Russia’s invasion of Ukraine in Feb. 2022 which damaged last year’s Q1 traffic and fares.

Ryanair’s Michael O’Leary, said:

ENVIRONMENT:

“Every customer switching to Ryanair from high fare EU legacy carriers can reduce their emissions by up to 50% per flight. We continue to invest heavily in new technology aircraft. During Q1 we took delivery of 21 fuel efficient, B737-8200 “Gamechangers” (4% more seats, 16% less fuel & CO2 and 40% quieter). In May, we signed a deal with Repsol to supply SAF to Ryanair bases in Spain. This builds on similar SAF arrangements with OMV, Neste & Shell and puts the Group on track to achieve its ambitious 2030 goal of powering 12.5% of Ryanair flights with SAF – with 9.5% already secured.

The most significant environmental initiative Ryanair can deliver near term, is to press for urgent reform of Europe’s inefficient ATC system. In May we submitted a petition to the European Commission, signed by over 1m of our customers, calling on the EU to protect “overflights” during national ATC strikes. We believe this would reduce flight delays, cut flight times, and unnecessary CO2 emissions. Over the past 6 months, French ATC alone, has held 60 days of strikes, during which the French Govt. used min. service laws to protect local/domestic flights while disproportionately cancelling overflights. We, and our customers, call on the EC President, Ursula von der Leyen, to protect the single market for air travel and minimise the impact of ATC strikes on EU citizens (while respecting the right of ATC unions to strike) by insisting that national Govt.’s protect overflights, as is already the case in Greece, Italy and Spain.

Today, we are proud to launch Ryanair’s 2023 Sustainability Report (“Aviation with Purpose”). Our recent $40bn order for 300 Boeing MAX-10 aircraft (21% more seats, 20% less fuel and 50% quieter) will enable us to pursue even more ambitious environmental targets over the next decade. We have reset our CO2 per pax/km target at a very ambitious 50 grams by 2031 (previously 60 grams by 2030). We have also published the Group’s 1.5 degree Climate Transition Plan.

SOCIAL:

As the Ryanair Group traffic grows to 300m p.a. by FY34, we expect to create over 10,000 new, well-paid, jobs for highly trained aviation professionals. To facilitate this growth as we take delivery of 90 more Gamechangers and 300 MAX-10s, we recently ordered 12 new CAE simulators (6 firm and 6 options worth over $120m). Building on the success of our new state-of-the-art aviation training centre in Dublin, we have finalised plans to develop 2 similar excellence centres to accelerate crew training in both Central Europe (Krakow) and the Iberian Peninsula. We are also upgrading our UK training centre in East-Midlands.

This summer, in anticipation of increased ATC disruptions, we invested heavily in operational resilience (increased crew ratios, doubled the size of our Dublin and Warsaw ops centres, enhanced our day-of-travel app. and continuously improving our live customer comms.) to ensure that our passengers and crew continue to enjoy Ryanair’s industry leading OTP and reliability. This investment has been rewarded with a strong Q1 CSAT score of 85% (up 2pts on our PY Q1), with “crew friendliness” continuing to be our top score (rated over 90%).

GROWTH:

We are operating our largest ever summer schedule (over 3,200 flights and up to 600,000 passengers daily). We have opened 3 new bases (Belfast, Lanzarote & Tenerife) and over 190 new routes, further growing our No.1 or No. 2 share in the Italian, Polish, Spanish and UK markets. We have recently announced plans to fly to/from Albania this winter, expanding our CEE footprint offering competition, choice and lower fares than the incumbent carrier. Structural EU capacity reductions following numerous EU airline failures or fleet reductions during Covid, volatile oil prices (discouraging weaker, unhedged, airlines from adding capacity), a shortage of aircraft (new and leased), the return of Asian traffic and this year’s very strong influx of American visitors to Europe (helped by a strong US$) means that European short-haul capacity remains constrained this summer. H1 demand is robust and fares remain ahead of last year as we move into peak S.23 although this trend seems weaker in Q2 than it was in Q1.

European airlines will continue to consolidate over the next 2-3 years, with the takeover of ITA (Italy) and the sale of TAP (Portugal) already underway. The large backlog of OEM aircraft deliveries is likely to constrain capacity growth in Europe for at least the next 4 years, which will enable Ryanair to further extend our market share gains as we take delivery of almost 100 Gamechangers over the next 3 summers. Our unit cost advantage over EU competitors, fuel hedging, strong balance sheet and low-cost aircraft orders out to 2033, coupled with our industry leading operational resilience, creates significant growth opportunities for Ryanair over the coming years as we grow traffic to 300m p.a. by FY34.

Q1 FY24 BUSINESS REVIEW:

Revenue & Costs

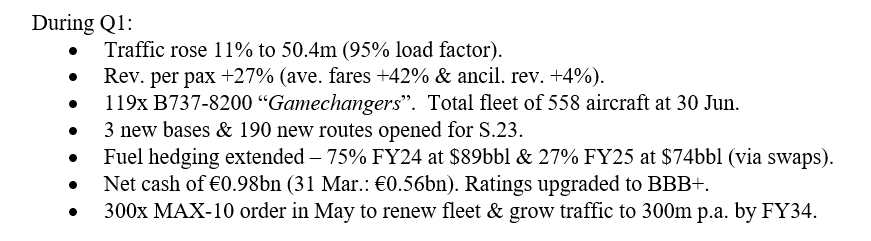

Q1 scheduled revenues increased 57% to €2.47bn. Traffic grew 11% to 50.4m and ave. fares rose 42% to €49 thanks to a strong Easter (the PY Q1 was badly damaged by the Ukraine invasion of Feb. 2022) and an extra UK (Coronation) public holiday in May. Ancillary revenue increased 15% to €1.18bn (c.€23.30 per passenger). Total Q1 FY24 revenue therefore rose 40% to €3.65bn. Total operating costs increased 23% to €2.94bn, primarily due to higher fuel (+30% to €1.34bn), staff costs (reflecting restoration of pay cuts, pre-agreed pay increases and higher crewing ratios as we invest in op. resilience) and higher ATC fees (incl. in airport & handling charges). Despite a modest increase in unit costs (ex-fuel) to just under €32 in Q1, Ryanair’s cost advantage over EU competitors continues to widen.

FY24 fuel requirements are almost 85% hedged at approx. $89bbl (with a mix of swaps and caps) and FY25 hedging has increased to 27% at approx. $74bbl. Over 90% of FY24 €/$ opex is hedged at 1.08 and approx. 50% of FY25 is hedged at 1.12. Our B-8200 “Gamechanger” order book is fully hedged at €/$1.24 (locking in significant cost savings as we take delivery of these more fuel efficient and quieter aircraft).

Balance Sheet & Liquidity

Ryanair’s balance sheet is one of the strongest in the industry with a BBB+ credit rating and over €4.8bn gross cash at quarter end, despite over €1bn capex. Net cash increased to €0.98bn at 30 June (€0.56bn at 31 Mar.). Substantially all of the Group’s B737 fleet is unencumbered, which significantly widens our cost advantage as interest rates and leasing costs continue to rise for competitors. We are on track to repay our second 2023 bond of €750m as it falls due in Aug. and €2.8bn FY24 capex (incl. peak Gamechanger capex and a MAX-10 signing deposit) from internal cash resources.

Our Board strategy, as our business recovers, is to firstly prioritise pay restoration and multi-year pay increases for our people. Secondly, we will pay down maturing debt as it falls due over the next 3 years, while at the same time funding our ambitious aircraft capex, from internally generated cashflows. Once we are confident that we can fully fund these large commitments, the Board will then consider restarting modest returns to shareholders, who supported Ryanair during the Covid pandemic. We are conscious that our shareholders invested just over €400m during our Sept. 2020 share placing (during the depth of the Covid crisis), and this was key to Ryanair subsequently issuing an €850m bond which helped us to survive the devastating impact of the Covid pandemic on travel.

FLEET:

Our Gamechanger fleet stood at 119 at quarter end and we expect to increase this to 124 by the end of July. We expect to take delivery of 49 B-8200s (173 in total) by year-end (Mar. 2024). As previously noted, Boeing has suffered multiple supply chain challenges, causing repeated delivery delays. We have worked closely with Boeing to minimise these delays, and the disruption to our schedules and traffic targets. We had originally expected 51 aircraft deliveries on/before 30 April, but the last of these deliveries was delayed into July. We hope that our winter 2023/spring 2024 deliveries will be less impacted, but already there are indications from Boeing that some deliveries may be delayed from April 2024 to June 2024.

In May, Ryanair signed an order with Boeing to purchase 300 Boeing MAX-10 aircraft (150 firm and 150 options) which, subject to shareholder approval at our Sept. AGM, will deliver between 2027 and 2033. These aircraft have 39 more seats (228 v 189 on the Boeing 737NG), but deliver 20% lower fuel consumption, 20% less CO2 emissions and are 50% quieter. The additional seats, apart from increasing revenue growth, will further widen Ryanair’s unit-cost advantage over European competitors for the next 20 years. We expect up to 50% of the order will be used to replace older NGs, while the remainder will facilitate controlled (but slower) traffic growth to approx. 300m p.a. by FY34. Given the strength of the Group’s balance sheet, we anticipate that most of this capex will be funded primarily from internal resources (although the Group will remain opportunistic in its financing strategy).

OUTLOOK:

We expect FY24 traffic to grow to approx. 183.5m (up 9%), which is slower than the 185m originally expected, due to Boeing delivery delays in spring and in autumn 2023. While the cost gap between Ryanair and competitor airlines continues to widen, as previously guided, we expect to see an increase of approx. €2 in ex-fuel unit costs this year due to annualised crew pay restoration, higher crew ratios, increased ATC & route charges and the impact of Gamechanger delivery delays. While Q2 bookings are strong, the fare increase in Q2 will be much lower than in Q1 due to much stronger PY Q2 pricing in FY23 when peak summer travel snapped back strongly following the Ukraine invasion. We currently expect Q2 fares will be higher than the prior year Q2 but by a low double digit percentage. We noted a softening in close-in fares in late June and early July. The final H1 outcome is, therefore, highly dependent on close-in Aug. and Sept. bookings. As is normal at this time of year, we have very limited Q3 visibility and zero Q4 visibility. Having enjoyed a bumper Christmas and New Year travel period last year (the first festive travel season that wasn’t curtailed by the Covid pandemic), we are conscious that consumers may require some fare stimulation to fill our 25% greater seat capacity this winter (compared to pre-Covid) following months of rising mortgage rates and consumer price inflation. If this transpires, then Ryanair’s load active/yield passive strategy, coupled with our industry leading cost base, will uniquely position our Group to capture further market share, albeit at lower fares this winter.

Despite uncertainty over H2 Boeing deliveries, accentuated recently by the collapse of a Yellowstone River bridge in Montana, a significantly higher fuel bill (up €1bn over last year), volatile oil prices for our unhedged fuel, very limited H2 visibility and the risk of tighter consumer spending this winter, we remain cautiously optimistic that FY24 PAT will be modestly ahead of last year. It is, however, still too early to provide meaningful FY24 PAT guidance. We hope to be in a position to do so at our H1 results in Nov.”

Related News

RYANAIR LAUNCHES PRAGUE – PAPHOS & KOSICE ROUTES

Ryanair, Europe’s No.1 airline, today (1st August) celebrated the first flight from Prague to Paphos, while on Monday (3rd August) it will launch a twice weekly service to Kosice, both as part of its extended Summer 2020 schedule.

To celebrate its new routes, Ryanair has launched a seat sale with fares from 729 Kc for travel to Kosice and from 759 Kc to Paphos, both until the end of October, which must be booked by Wednesday (5th August), only on the Ryanair.com website.

RYANAIR LAUNCHES PRAGUE – PAPHOS & KOSICE ROUTES

Ryanair, Europe’s No.1 airline, today (1st August) celebrated the first flight from Prague to Paphos, while on Monday (3rd August) it will launch a twice weekly service to Kosice, both as part of its extended Summer 2020 schedule.

To celebrate its new routes, Ryanair has launched a seat sale with fares from 729 Kc for travel to Kosice and from 759 Kc to Paphos, both until the end of October, which must be booked by Wednesday (5th August), only on the Ryanair.com website.